Image by Andrew Cebulka via Stocksy

"When I was trying to buy my first home, I wasn't buying smashed avocado toast for $19 and four coffees at $4 each."

At first glance, this seemingly hyperbolic statement sounds like a nugget of outdated wisdom from your wise-cracking, out-of-touch grandpa (who also happened to walk uphill both ways to and from school as a young boy).

And while your normal response might be to take another sip of your iced almond milk latte, nod, and give a patronizing smile, this quote is harder to ignore when it’s coming from the mouth of a fabulously wealthy real estate expert.

So when real estate magnate and multi-millionaire Tim Gurner spouted this quote to the Australian version of 60 Minutes last month, the Internet had a bit of a freak-out. Nearly every millennial on the housing market flared up with an opinion. And why not? It seems that, ever since the first round of millennials began peeking their heads into the perilous real estate market, they’ve gotten nothing but flack.

The Dreaded Down Payment

Image Courtesy of TheOklahoma100.com

Defined as the generation born between 1981 and 1997, Millennials are notorious for being a confusing buyer demographic. Their real estate habits (or lack thereof) have left experts scratching their heads, wondering why such a massive well of potential buying power just can’t seem to commit to a white picket fence.

Experts and economists have speculated to no end, but it seems that if you go straight to the source, millennials have an overwhelmingly consistent answer: “I know buying is the smartest option...I just can’t afford a down payment.”

According to Tim Gurner, the real problem behind this lies in misplaced spending (particularly, on delicious and expensive avocado toast). But is this really the issue? According to one study, Millennials DO spend a greater percentage of their daily budget on “splurge-worthy” purchases (like sandwiches and coffee) than previous generations. However, in almost every other category, millennials prove themselves thrifty. The average U.S. consumer doles out $32,000 annually on miscellaneous purchases like apparel, entertainment, and regular bills. Millennials, on the other hand, manage to keep this number down to $26,000.

Sorry, Tim. It looks like the millennial housing market issue is a little more complex than expensive toast.

So why are Millennials struggling to save? The real answer may be more mental than monetary. While many would begin to point to student debt and a “recession mindset” as main blockades in the pursuit of a down payment, research has found that Millennials are either uninformed or misinformed when it comes to their own financing options.

Dispelling the Myths

In a recent survey, 42% of Millennials said they didn’t know what lenders expect of them, and 73% were unaware of low downpayment options. The most commonly touted myth is that every buyer needs to be ready to pay 20% up front…a sum that (according to Gurner’s logic) would cost you over 5,000 pieces of avocado toast for a mid-priced San Antonio home.

The truth? A hefty down payment is only necessary if you’re trying to avoid mortgage insurance on a conventional loan. And according to the National Association of Realtors, first-time buyers only put down an average of 6% for their initial real estate venture! Depending on your situation, many lenders are willing to underwrite loans with down payments as low as 3%. To prove it, RealtyTrac estimates that about 30% of all homebuyers put down 3% or less on the cost of the home.

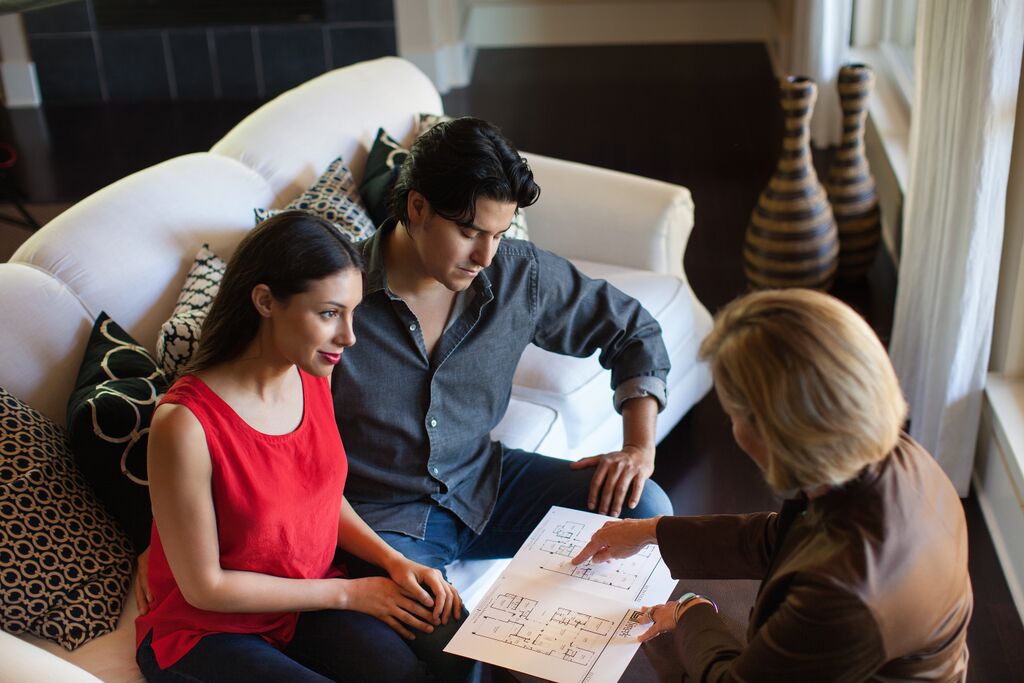

If you're interested in finding out more, we recommend downloading our exclusive Buyer’s Guide, contacting an expert agent, and getting connected with a lender. In the meantime, we’ve listed a few alternative types of loans and services that help with that initial upfront cost.

FHA Mortgage

This type of loan was designed for the buyer unable to qualify for a conventional home loan, making them popular amongst first-time buyers. Instead of a hefty down payment, these loans offer up to 97% of the value of the home, and the 3% down payment can come in the form of a gift or grant.

VA Mortgage

It may sound too good to be true, but VA Mortgages require no down payment or monthly mortgage insurance. The kicker? Eligibility depends on current or former military service. (Ask a lender if you think you may be qualified & check out this list of affordable houses near military bases!)

Alternative Conventional Loans

HomeReady™, Home Possible® Advantage, and Conventional 97 are a few examples of loans that lighten loan requirements, reduce mortgage insurance, etc.

USDA Home Loans

Created for single-family home buyers in more sparsely populated areas, USDA home loans don’t require a down payment. Check with your lender, as eligibility is location-based (usually limited to homes outside of major metro areas).

Piggyback Loans

Sometimes known as 80/10/10 or 80/15/5 loans, this type of loan involves the borrower taking out two loans simultaneously: one for 80% percent of a home's value, and the other to make up for whatever cash is lacking to make up a 20 percent down payment (removing the need for mortgage insurance).

Down Payment Assistance (DPA) Programs

Mostly facilitated by government institutions and nonprofits, these programs offer gifts and no-interest loans to support homeownership. Nearly 90% of all single-family homes in the U.S. are eligible for some kind of DPA, according to a study by RealtyTrac!

We understand: while still far less than a 20% down payment, 5% of your first home is still a hefty sum of money...and we certainly endorse smart and healthy budgeting skills. By taking advantage of a few strategic local penny-pinching strategies, you can save quite a chunk of change! We recommend exchanging that piece of artisan avocado toast for a street taco (cuz they’re better, anyway) and heading to your local happy hour instead of indulging in a late night, full-price cocktail.

Thankfully, one of the biggest advantages of living in San Antonio is the affordability factor. To prove it, we’ve listed a few affordable properties around the city...and just for fun, we’ve also calculated how much avocado toast ($8) it would take to put down a 20% down payment on each!

106 Lakeshore Dr: $113,000

20% Down Payment: 2,825 pieces of avocado toast

Neighborhood: Alamo Heights

27843 Papoose Pass: $135,000

20% Down Payment: 3,375 pieces of avocado toast

Neighborhood: Timberwood Park

9738 Green Plain Dr: $139,990

20% Down Payment: 3,498 pieces of avocado toast

Neighborhood: Heritage Park

5127 Stockman Dr: $144,900

20% Down Payment: 3,622 pieces of avocado toast

Neighborhood: Ranchland Hills

434 Zachry Dr: $152,000

20% Down Payment: 3,800 pieces of avocado toast

Neighborhood: Donaldson Terrace

5702 Spring Moon St: $160,000

20% Down Payment: 4,000 pieces of avocado toast

Neighborhood: Spring Creek Forest

7015 Elusive Pass: $165,000

20% Down Payment: 4,125 pieces of avocado toast

Neighborhood: Raintree

From the most popular neighborhoods to the outlying properties, The Alamo City’s low cost of living is incredibly alluring to young buyers...leading millennials to move here in lieu of pricier Texas cities like Austin, Houston, and Dallas. If this describes you, we’d love to help you navigate the San Antonio real estate market! Download our exclusive Buyer’s Guide here, and contact an agent today to get started.